The Argentinian hyperinflation: Is Milei Paving the Road to Stability?

Dollarization: A solution or a risk?

Newly elected president Javier Milei has plans to dollarize

The new government directed by the renowned economist, Javier Milei, rose to power with the promise of reducing inflation and maintaining a fiscal surplus, in order to be able to adopt ‘dollarization’ as a solution. The austerity policies that have been and will be implemented by Milei with this goal in mind will greatly hurt the Argentinian economy in the short term. Milei describes these changes as short term sacrifices that are to be made, in order to suffer less in the long run.

Recent history of hyperinflation in Argentina

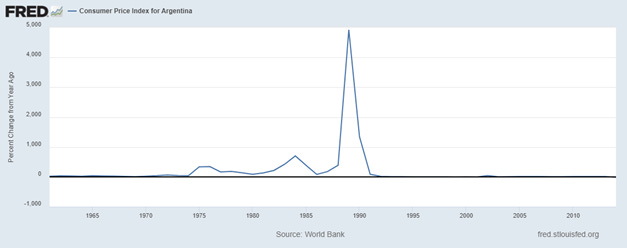

For decades, Argentina has struggled with high inflation and economic volatility, of which the most extreme levels experienced during the hyperinflationary period of the late 1980s and early 1990s. The highest annual peso depreciation recorded during this period was approximately 3079.81% in 1989. The hyperinflationary spiral was fueled by a combination of factors, including excessive money printing to finance government spending, large fiscal deficits, external debt crises, and economic mismanagement. In 2023, Argentina's annual inflation rate was 211.4%, which is the highest it’s been since the reform of the early 1990s.

This FRED graph with Annual Change in CPI in Argentina has observations from 1961 to 2014, in units of percent change from a year ago (a measure of annual inflation). Notice that the range on the

y-a xis has a maximum of 5000, which is why it is difficult to discern lower rates in the late 2000s and early 2010s. We recommend curious readers to take a look at this WorldData webpage that has Argentina’s annual inflation rates from 1980 to 2022 and a nifty peso depreciation calculation tool.

On the concept of dollarization

Hard- and soft dollarization are two versions of a country's use of foreign currency alongside or instead of its domestic currency. Hard dollarization is a complete replacement of a country's domestic currency with a foreign currency, typically the US dollar or the euro, as legal tender for all

transactions within the economy. Because the central bank has no control over monetary policy or the supply of money in this foreign currency, essentially, the country relinquishes control over its monetary policy to the country whose currency is being used. Soft dollarization is a situation in which the foreign currency circulates alongside the domestic currency as a medium of exchange and store of value. Unlike hard dollarization, the domestic currency remains legal tender, and the central bank retains control over monetary policy.

Advantages of hard dollarization for Argentina include increased monetary stability, reduced exchange rate uncertainty, and enhanced credibility in the eyes of international investors. The main disadvantage for Argentina could be the loss of control over monetary policy, which can limit the ability of policymakers to respond to domestic economic conditions. Ecuador and Panama have adopted hard dollarization. However, this has been under different circumstances than Argentina has now, such as a notably less worse state of the economy and a very strong trade relationship with the US, which made it additionally practical to adopt the dollar.

A big advantage of soft dollarization could be reduced exchange rate volatility, together with enhanced confidence in the stability of the domestic currency, and increased access to international markets. However, a disadvantage is that it complicates monetary policy management even more, as the central bank may need to consider factors such as exchange rate movements and foreign currency reserves in its policy decisions. Soft dollarization is a way to describe what the restructure of the early 1990s , The Convertibility Plan, did for the Argentinian economy, in which the worth of the peso was pegged to the US dollar.

The debate on Milei’s vision

Milei’s long term goal centers around abolishing Argentina’s Central bank, as he has expressed many times, that he believes that the main reason for Argentina’s failing economy lies on the poor management done by the entity. Milei has said that “eliminating the central bank is essential”. He sees the BCRA as inflation-stoking. Their response to economic adversities always reduces to printing more money which continuously fuels the problem. To achieve this abolition, he needs to gradually convert at least two thirds of the monetary base to US dollars. Economists say that the Argentinian government currently doesn't have enough dollar reserves to achieve hard dollarization. Because Argentina needs to have a sufficient reserve level, Milei´s plan includes extreme and strict austerity measures. These hard but necessary measures bring a lot of cons to the stabilization plan, consequently creating a lot of arguments against this switch, leading to a divide about whether the switch should take place at all. For oversight, we have divided them by general topic in the 5 sections below.

1. Austerity

The adoption of high interest rates, currency devaluation, and reduced government spending all contribute to a decline in business confidence in the short term. This triggers the ‘Crowding Out Effect’, discouraging private sector consumption and potentially spiraling into recession if not managed carefully and over time. As businesses and private investors reduce consumption, unemployment rates rise sharply, further impeding economic growth and exacerbating uncertainty and instability.

However, when contractionary policies are implemented abruptly and aggressively, the government seeks to minimize their impact. Milei aims to implement the austerity measures aggressively, however he faces political obstacles in doing this so far, as the president is struggling to overcome hostile lawmakers to enact his radical austerity agenda.

Since the plan of dollarization centers on using the federal reserve to finance the change, there has been a heavy focus on cutting back government expenditure. When doing this they not only stop programs that are beneficial to society and support less favored social classes but also increase unemployment from all the people being fired from government funded jobs, which by the multiplier effect also slows down growth in the economy. Ultimately declining social welfare and satisfaction amongst the population.

Inflation has been cut in half from 25% in December to 13% in February, and the government achieved a fiscal surplus in January and February based on almost entirely stopping public works and a notable reduction in pension payouts.

2. Interest rates

In March 2024, Argentina's interest rates stood at 80 percent, down from the previous level of 100 percent. Under normal circumstances, such interest rates would be unthinkable. However, even at these levels, interest rates still hold a negative real value. This means that despite an 80 percent interest rate, the purchasing power of money is eroding faster than the interest earned. Each passing day sees inflation increasing at a higher rate than the set interest rate, by the ongoing austerity modifications. This creates a complex situation where, despite extreme austerity measures, consumers are still incentivized to spend, worsening the country's inflationary distress.

3. IMF and debt rates

All these potential shortcomings and inadequacies in monetary policy implementation prompt a closer examination of Argentina's current debt situation. The country grapples with years of accumulated deficits, compounded annually, highlighting the crucial role of the International Monetary Fund (IMF) in assisting Argentina as it endeavors to free itself from its financial predicament.

One of the main goals of Milei’s economic policy is to reduce the countries debt, and to do this hasn’t just limited itself to monetary and fiscal policy, but it reached out to the IMF to ask for a central bank financing of government debt loan of 44 billion dollars, this would help the countries international reserves and smooth the process of converting to US dollars. Argentina has had a hard time trying to manage its debt levels relative to its economic output. Therefore, the country sought assistance from the IMF to address these debt crises. The IMF gives standby loan arrangements to certain countries to stabilize their economies. Argentina thankfully made use of these arrangements securing $56 billion dollars from the IMF in 2018. Despite this being one of the largest assistance the IMF ever gave, the country continued facing economic challenges including the growing high inflation rates the country has been struggling with again, since the second half of the 2010s.

The debt sustainability still remains to be a complex issue keeping the government, creditors and IMF busy discussing and negotiating. The IMF is promoting stability and sustainable growth in countries

with economies like Argentinas, by giving financial assistance and policy advice, thus the reaction of the IMF to Milei’s new monetary policies have been positive and extremely supportive.

4. Monetary policies

The sharpest and most polemic monetary policy taking place, as people were warned by Milei himself, is the decrease of the exchange rate between the peso and the US dollar. In order to convert all reserves of the central banks to pesos, the government needs to fix a manageable exchange rate between currencies. However, due to the current quantity of pesos in exchange, they will need to have an artificial devaluation of the currency to almost 50% of its current value to be successful at it, decreasing the current purchasing power of the argentinian population instantly.

This policy generated a lot of controversy amongst the population, since the goal is to stabilize the economy. To stabilize, Milei argues they do need to weaken the economy by devaluating the peso first. It needs to get worse in order for it to be better later.

5. The end goal: hard dollarization

While having a hard dollarization in place can result in a stronger economy overall, it's important to acknowledge that uncertainty accompanies its proper implementation. Additionally, even if executed correctly, hard dollarization brings along a plethora of considerations that prompt reflection on whether it truly aligns with the long-term needs of the Argentinian economy.

For a country to be eligible for dollarization, it has to follow very certain specific conditions, as JPMorgan strategist Michael Cembalest explained in a

Does dollarization assure a stable economy for the future?

The effectiveness of dollarization presents a multifaceted challenge, encompassing technical economic landscapes, policy ramifications, and social implications. Argentina's historical struggles with hyperinflation, coupled with the necessity for austerity measures and the loss of control over monetary policies, have rendered the dollarization process less functional and more challenging to integrate fully into the economy.

| A guest post by

|

| A guest post by

|

| A guest post by

|